Saving for the future is something most people know they should do, but the best ways to do it are not always as clear. In addition to our annual list of the area’s top financial professionals as named by their peers, we gathered tips from some of the winners to help you strategize and save.

Life or Death

We break down elder care and what you need to know about it right now.

–Robyn Smith

Let’s say today is a completely normal day, but then tomorrow your spouse is diagnosed with dementia, or one of you gets cancer—suddenly, you need round-the-clock care. It might not seem like it, but that day is coming a lot sooner than you think, and it’s good to know what you and your children need to prepare for, whether it’s life insurance, a long-term care policy or both. Your quality of life is worth the hefty premium.

Rose Price, a certified financial planner with VLP Financial Advisors, defines elder care as more than just insurance. She looks at all aspects of someone’s financial situation and gives them options suited to their needs, whether they need round-the-clock care, which can be up to $20,000 a month, or just a solid support system nearby.

“It’s a very delicate situation, very hard, especially if the children aren’t local or are not involved, because then they’re at this point where a lot of the time they have to make this decision on their own,” Price says. Clients who can’t afford to pay the premium or wish to discontinue are encouraged to ask their children to pay it. It’s a lot easier to pay the premium now than struggle to find a way to pay when you need care the most. Also, if you don’t use the insurance, in many circumstances the care is passed down to your family.

According to Price, group policies are a good option for those who want to save money, but even just having a joint policy shared between spouses is a good way to reduce the premium by 30 to 40 percent. The earlier you begin to pay the better because once you need care, insurance companies are less likely to offer you policies.

“If you have cancer, you could possibly get [a long-term care policy], but you couldn’t get life insurance because cancer kills you; it doesn’t put you in a nursing home,” Price says. “If you have dementia, you’ll be able to get a life insurance policy because you might live forever and just not know it. But long-term care will say, ‘Eh, that looks really expensive.’”

Those who can’t afford insurance can qualify for Medicaid, but this is a long and tricky process. Price encourages state-dependent clients to seek out specialists and local resources to receive the best quality care. It’s important to find someone who can look at your whole financial picture and give you all your options.

“There are resources out there. Familiarize yourself with the local government—not only the county, but also the state because there are more [resources] than people know,” Price says. “They just don’t know where to start.”

Rising Spenders

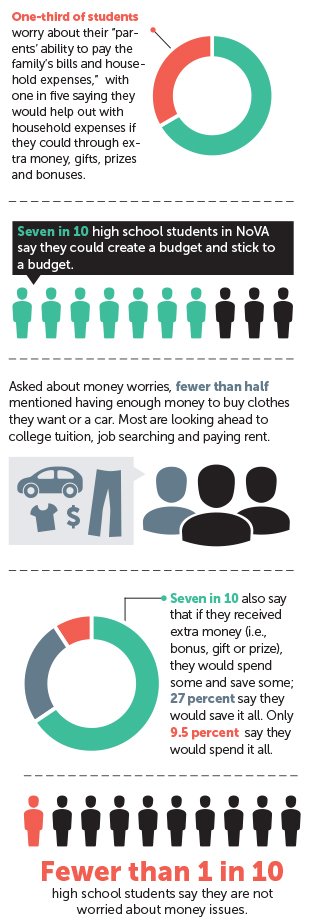

Earlier this year Apple Federal Credit Union surveyed 4,240 Northern Virginia high school students about money matters. A look at their responses shows a lot about today’s personal finance situations and what this generation has planned for the future.

Source: Apple Federal Credit Union, May 2015 survey

Retirement 101

A Q-and-A with Kim McLeland, president of CJM Wealth Advisers.

By Robyn Smith

When most people think of retirement, they think of long days on a grand Floridian beach, an endless stream of martinis and fruit trays at their fingertips and, in the distance, the sound of grandchildren laughing and waves crashing against the serene shore. Few consider the substantial finances required to support this leisurely lifestyle, but it’s never too early to consider investing in an individual retirement account or 401(k) plan. To help navigate the options, Kim McLeland, president of CJM Wealth Advisers, Ltd., gives the inside scoop on how and when people should put a little green behind that blue fantasy.

How much do people need to save for retirement in this area?

It really depends on what their retirement goal is. There are old yardsticks that talk about people needing perhaps 70 percent of what they’re living on now—that’s what they’re spending, not necessarily their income—but sometimes people change. Sometimes people move back to communities that perhaps they had grown up in, so the real definition of what people need to achieve their goals is a little harder to come up with than any of us would like. I would say that what people need to do is try to estimate what expenses they’re going to have when they’re retired, and then one can see what we think they would inflate between now and the time they’re retired and begin to come up with a plan to have an appropriate lump sum out there in the future.

If we were to simply say we need a sum of capital on which we can draw a certain amount to cover the expenses and be reasonably sure that we won’t outlive our money, then I would tell you that whatever expenses need to be covered in the future, I would be inclined to divide them by 4 or 5 percent and use that as a means of calculating the lump sum they would need at the time they retired.

That’s a lot.

It is. Now, it could be less if someone was willing to go ahead and say they had no desire or no interest in having any beneficiary receive anything from them. It really does take a fair amount if you want to be sure that there is something left at the point where you don’t need it anymore. How far back from that scale you can step is kind of hard to figure out. It can be quite a bit of money.

By beneficiary, do you mean leaving money for your children and other people in your life after you go?

Yes. Keep in mind that whatever expenses have to be covered, we can actually reduce them by what we might project social security would cover. We still have a social security system—for young people, it’s likely to be modified in the future. For people who are, let’s say, 50 or older, it’s probably not going to impact too much, so there is a portion that would be covered by social security and their capital, whether it exists in a portfolio that they have saved themselves, on an after-tax basis or whether it is in an IRA or 401(k). Those are the remaining dollars that would have to make up the difference. You really have to look at all of those things in order to come into a sense of what’s really possible.

When should a person start seriously saving for retirement?

Well, the financial planner would tell you when they collect their first paycheck. As a practical matter, there are relatively few people who start that early. I remember running an illustration with some Boy Scouts some years ago when I was teaching a personal finance merit badge, and I had them take a look at two things in particular, but one of them bears on the retirement aspect. I had them calculate a future amount of money that would be available to people. Under the first scenario, the worker started immediately: first job at 22, they saved an amount in their IRA every year, but they could only do it for 10 years. The other person basically did the same thing but didn’t start until 11 years into their career. What the Scouts found when they ran those calculations was the person who ran the first 10 years and stopped had more money at 65 than the person who began 11 years later and throughout the time was earning the same return on their investments as the first one. Even though the second person invested more out of pocket, the first person benefitted from having it compounded over a longer period of time. That really woke them up for at least the rest of that meeting.

So even if you invest more later in your career, it’s still better to have your IRA grow over a longer period of time?

You ask a critical question there: Which is more? So in my example, there was more being invested, but they were only investing the same amount each year as the person in the first instance.

Most people do invest more over time rather than a constant dollar amount, but that is really what it takes to make up for years where you didn’t have something compounding for your benefit. That could be because you were choosing to work in a field that was really hard to get started in, but it could also happen if you were faithfully doing it but we had a nasty period where the stock market didn’t provide adequate returns. We’ve certainly seen such nasty periods in the past 20 years.

That’s a good point. I assumed that most people would make more money 11 years into their career than when they first start out.

You’re absolutely right. If you had phrased it slightly differently—When do most people put the most amount of money away?—my answer to you would be, if they had been parents, when their youngest graduates from college. Because up to that point, there are extra stresses and strains on the household budget, and after that point, there’s more flexibility. That flexibility would allow them to spend some money on themselves that previously they weren’t able to, but it may also allow them to fully fund the contributions to their retirement plans that maybe before they were not able to do.

That would make sense as the ideal time because that’s when you focus more on yourself rather than your children or your family in general.

I think so. Plus they’re closer to when they are starting to think about, as I sometimes put it, “What do I want to be when they grow up?” If you’ve met your obligations to your family, then you may have a point at which you can say, “What is it that I really want to do with the rest of my life?” And when you settle upon the answer to that, that may give you a spur to invest more heavily to make sure you’re more financially prepared for the rest of your life.

What should people do now, no matter how old they are, for their retirement savings?

Am I allowed to give you a one-word answer? Start. I think that the key is to start and never become discouraged about continuing.

Is there anything people should know, even if they’re not thinking about it right now?

I think that there is very much a key element, and let me put it in the context of an analogy: If there was something that you needed for a dinner that you particularly like in your household, or if there was some item of clothing that you really needed to have your wardrobe and you reached a point where it was time to go shop for either of those, and you got to the store and found that they were on sale, and they didn’t cost as much as you thought you were going to have to pay—I think most people would smile and think that was wonderful. Would you agree?

I think I would.

Now when the stock market falls, nobody likes the fall, but if what you were investing in before was really something good, the fall would mean that you would be able to buy the thing that you previously thought was good for less. And by putting the same amount of money into the investment as you were before the fall, you end up buying more shares of that investment. Over a long term, success in many respects can be dependent on the purchase of those extra shares. We’ve seen very, very wide swings in the market—likely to see them again in the future. But the continuous commitment of money is what really keeps one on their target and ultimately helps them reach their target. I think that’s really key.

College Saving 101

Ensure that your family has the right financial tools for sending your children to college.

By Rachel Sandler

Gregory S. Smith of the Wise Investment Group tells Northern Virginia Magazine how families can best approach saving for college.

Tuition vs. retirement savings for parents.

According Smith, families need to establish goals and priorities when contemplating how to allocate their limited resources when saving for retirement and college. “Some parents would rather eat glass than not be able to pay for college for their children,” Smith says. Parents who chose to focus on college savings instead of retirement need to be prepared for the possibility of working longer than expected or spending less money in retirement. Others might want to focus on retirement because loans are available for students. The most important thing, though, is to plan how your family’s goals can be met, no matter what they may be.

Student loans

The first step families should take is filling out and submitting the FAFSA form, which will tell you what federal loans are available to you. One piece of advice that Smith usually gives clients who are thinking about taking out student loans is that even though a specific dollar amount might be available, some might not need all of that money. It’s important to know how much money you need and how much debt to take on so you don’t end up borrowing more than necessary.

When starting to pay student loans back after graduating, Smith says clients often don’t know that they might exceed the threshold for tax-deductible interest rates. “Know where the limits are for being able to deduct student loan interest,” Smith adds.

State college savings plans

There are plenty of resources that have information on college savings plans, or 529 plans, available in your state. According to Smith, savingforcollege.com is a great website that will give you a list of the 529 plans offered in your state along with details about the investment, cost and tax information. There are also a multitude of other avenues that families can use for college savings in addition to 529 plans. Prepaid tuition plans, Coverdell IRAs, custodial accounts or a post-tax account in your name, only titled in such a way so as to remind you on every monthly statement that the account is to be used specifically for education purposes, are some of the other choices available. According to Smith, the best way to wade through all of the options is to meet with a certified financial planner practitioner. Most of the time, a combination of savings plans is needed for more flexibility, Smith adds.

Have a rainy day fund.

“Make sure you’re adequately insured, and make sure you have the appropriate emergency funds available so if you are ever unemployed or if an emergency does come up, you aren’t forced to sell investments.” –Gordon Bernhardt, Bernhardt Wealth Management, Inc.

Understand your goals and expectations for retirement.

“When we’re having the retirement planning conversation related to long-term care and asking clients to picture what they look for in retirement, they usually picture things like travel, more time with family, leaving a legacy and things that bring them comfort and happiness. What we try to articulate is that there may be some things that they don’t think about. For example, if one of your goals in retirement is to not rely on a loved one for care, then we need to take some specific steps now to help get you there. People don’t necessarily think about that as a retirement goal unless they’re prompted to do so.” –David Hillelsohn, Haslett Management Group

Start saving for retirement early.

“I encourage every young person once they graduate from college to get in the habit of putting aside and saving 10 percent for retirement. If we all saved 10 percent at the beginning of our careers, I believe that everyone would have a higher probability of retiring in the lifestyle they want and having a happy and comfortable lifestyle. There’s something magical about 10 percent.” –Gordon Bernhardt, Bernhardt Wealth Management, Inc.

Healthy people can get better life insurance terms.

“People often who are very healthy can often obtain life insurance with more favorable rates—sometimes with a 10, 20 or 30 year premium guarantee and something that’s portable. This means that you retain the insurance regardless of who you work for. When you’re evaluating employer-sponsored life insurance plans, it makes sense to consider insurance outside of the employer-sponsored benefits for portability.” –Kim Natovitz, The Natovitz Group

Keep emotions out of investing.

“I always encourage people to keep their emotions at the door. Don’t panic when things are scary, and don’t get greedy when things seem to be going great and the market is just going gangbusters. Our emotions are our worst enemy.” –Gordon Bernhardt, Bernhardt Wealth Management, Inc.

Think differently about budgeting while in retirement.

“It is important that clients recognize that they’re going to take away some expenses in retirement and that they’re going to add some others. For example, they’re going to spend more on chores and upkeep of the house; they’re going to spend more on travel and vacation; they’re also going to spend more on health care. As we look to budget for specific long-term health care needs, we do ask people to identify how much they think they’re going to have in income and what the shortfall is related to health care expenses.” –David Hillelsohn, Haslett Management Group

Plan, plan, plan.

“Study after study shows that those who focus on planning—planning for their retirement, planning for a child’s college education—are happier than those who don’t. They have more peace of mind and more security.” –Gordon Bernhardt, Bernhardt Wealth Management

Click to see Top Financial Professionals 2015

(September 2015)